Building genuine savings on a small income feels impossible to many people yet the habits and strategies that make saving consistently possible are available to almost anyone regardless of income level. This guide provides practical actionable approaches that work even when money feels tight.

Why Saving Matters Even With a Small Income

Many people with small incomes postpone saving until they earn more believing their current income is simply too small to make saving worthwhile. This reasoning misses a critical point. The habits and discipline developed through consistent saving on a small income are exactly the same habits that produce meaningful wealth when income eventually grows.

Building these habits early creates a foundation that scales naturally with income rather than requiring a completely fresh start later when supposedly better financial conditions finally arrive.

Track Every Expense Before Trying to Cut Anything

- Why Saving Matters Even With a Small Income

- Track Every Expense Before Trying to Cut Anything

- Apply the Pay Yourself First Principle

- Identify and Reduce Your Three Largest Expense Categories

- Create a Realistic Monthly Budget

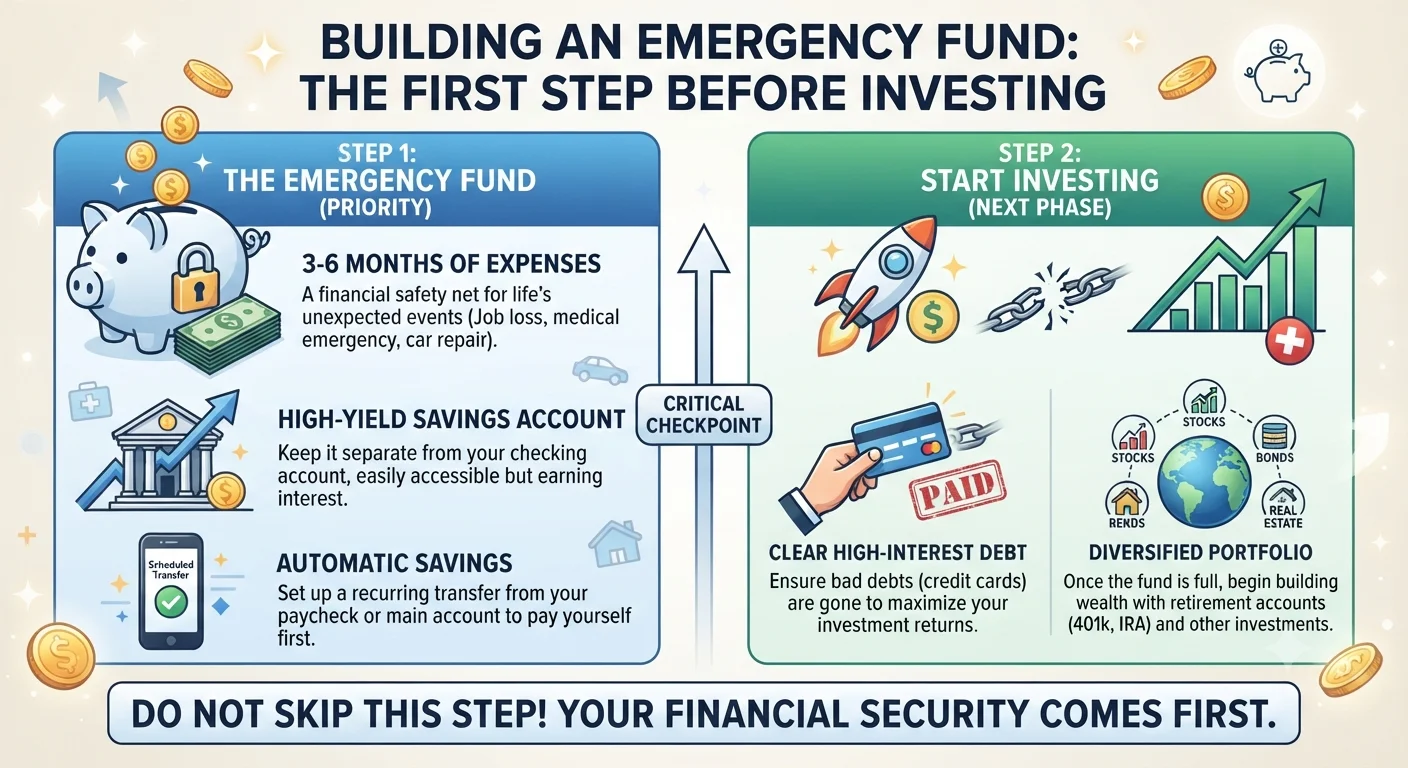

- Build an Emergency Fund as Your First Savings Priority

- Automate Your Savings Where Possible

- How Saving Connects to Your Trading Capital Goals

- Frequently Asked Questions About Saving Money

Before making any changes to your spending patterns spend at least two to four weeks tracking every single expense regardless of how small. This tracking exercise reveals where money is actually going rather than where you believe it is going which often produces surprising insights about spending patterns you had not consciously noticed.

Many people discover through this exercise that a significant portion of their income disappears into small frequent purchases that individually feel insignificant but collectively represent meaningful amounts over a full month.

Apply the Pay Yourself First Principle

Rather than saving whatever remains after all spending is completed decide on a specific savings amount before spending on anything else and transfer that amount immediately when income arrives. This approach ensures saving actually happens consistently rather than being repeatedly postponed as spending consumes available funds throughout the month.

Even a very small percentage applied consistently through this approach produces real accumulated savings over time. The specific amount matters less initially than establishing the habit of prioritizing saving before discretionary spending begins.

Identify and Reduce Your Three Largest Expense Categories

After completing your expense tracking exercise identify your three largest spending categories and evaluate whether any reductions are practical without significantly affecting your quality of life. Small reductions in large expense categories produce more meaningful savings impact than eliminating small expenses entirely.

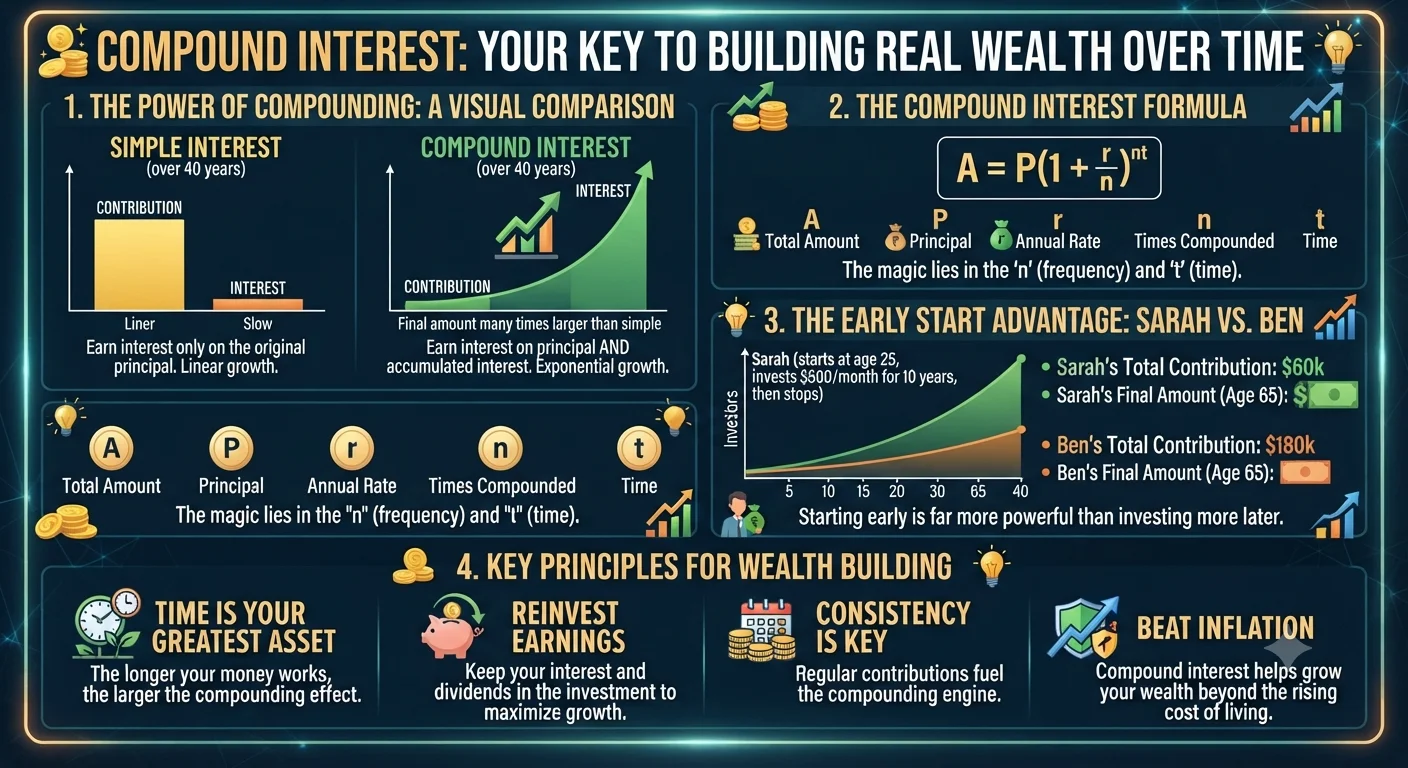

- What Is Compound Interest and How It Can Help You Build Real Wealth Over Time

- 10 Investment Mistakes That Beginners Make and How to Avoid Every Single One

- How Much Money Can You Realistically Make From Binary Options Trading Each Month

For example reducing a large monthly expense category by ten percent frees considerably more money than completely eliminating a small occasional expense even though the elimination might feel more dramatic psychologically.

Create a Realistic Monthly Budget

Build a monthly budget that allocates your income across essential expenses savings and discretionary spending with specific amounts assigned to each category. A realistic budget acknowledges your actual spending patterns rather than imposing unrealistic restrictions that will inevitably be abandoned within the first few weeks.

Review and adjust this budget monthly based on actual experience rather than treating it as a fixed permanent document since life circumstances and priorities change over time in ways that require corresponding budget adjustments.

Recommended Articles

INVESTMENT TIPS

INVESTMENT TIPS

INVESTMENT TIPS

INVESTMENT TIPS

INVESTMENT TIPS

INVESTMENT TIPS

INVESTMENT TIPS

INVESTMENT TIPS

Build an Emergency Fund as Your First Savings Priority

Before allocating savings toward investment or trading capital build an emergency fund covering at least three months of essential expenses. This buffer protects your investment capital from being withdrawn prematurely during unexpected financial difficulties and protects your overall financial stability from being disrupted by unavoidable unplanned expenses.

Without this emergency buffer even a modest unexpected expense can force you to withdraw money you had intended to invest which undermines both your investment plans and your savings momentum.

Automate Your Savings Where Possible

Automating your savings transfer removes the daily decision of whether to save this month making consistent saving a default behavior rather than something that requires renewed willpower each time. Even if automation is not available through your specific banking situation establishing a specific calendar day each month for your manual savings transfer creates a reliable routine that produces similar consistency.

How Saving Connects to Your Trading Capital Goals

Building consistent savings habits directly supports your trading goals by creating a sustainable source of funds to gradually grow your trading account over time without requiring you to risk essential money. A trader who saves a modest amount monthly specifically designated for trading capital development builds their account gradually in a financially sustainable way.

This approach is significantly healthier than depositing large amounts borrowed or needed for essential purposes under pressure to generate returns quickly which creates exactly the emotional desperation that undermines sound trading decisions.

Frequently Asked Questions About Saving Money

Is it possible to save meaningfully on a very small income Yes. Even very small consistent savings amounts produce meaningful accumulated results over time particularly when combined with the habit development that scales naturally as income eventually grows.

Should I invest before building an emergency fund Most financial guidance recommends building an adequate emergency fund covering essential expenses before committing significant capital to investment or trading to protect your financial stability from unexpected disruptions.

What percentage of income should I save each month Common guidance suggests aiming for at least ten to twenty percent of income though starting with whatever amount is genuinely sustainable and increasing gradually as possible is more effective than setting an ambitious target that proves unsustainable.

How do I save money when all my income goes to essential expenses Focus first on tracking every expense to identify where money is actually going then evaluate whether any genuine reductions in your largest expense categories are possible before concluding that saving is currently impossible.

How can saving money help my binary options trading Consistent saving creates a sustainable source of funds specifically designated for trading capital development allowing you to build your account gradually without risking money needed for essential living expenses.

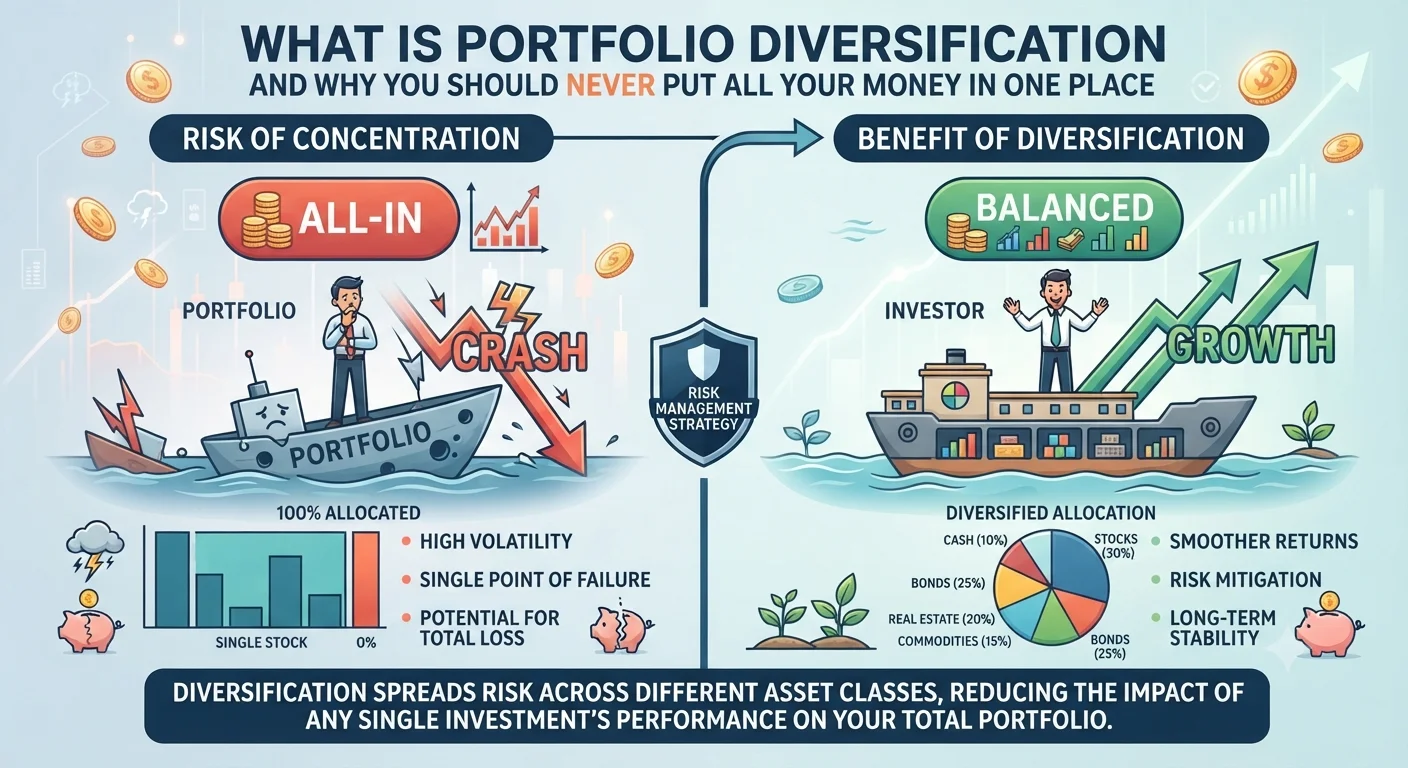

Knowing where to put your savings is just as important as building the habit itself. Continue reading our guide on what portfolio diversification means and why you should never put all your money in one place.

This article is for educational purposes only and does not constitute financial advice. Always make financial decisions based on your own specific circumstances and risk tolerance.