One of the most devastating experiences a trader can face is requesting a legitimate withdrawal and discovering that the platform is unwilling or unable to process it honestly. This guide explains exactly why some platforms refuse payments and what practical steps you can take to protect yourself and potentially recover your funds.

Why Some Platforms Refuse to Pay

Some binary options platforms operate with the deliberate intention of collecting deposits without ever intending to process genuine withdrawal requests. These fraudulent operations use various tactics to create the appearance of legitimate trading activity while systematically preventing clients from actually accessing their funds.

Other platforms may have genuine operational problems including liquidity issues or regulatory complications that prevent them from processing withdrawals even without deliberate fraudulent intent. While the outcome for the affected trader is similar the appropriate response and potential for recovery may differ depending on the underlying cause.

Common Tactics Used to Delay or Refuse Payments

- Why Some Platforms Refuse to Pay

- Common Tactics Used to Delay or Refuse Payments

- Step One Document Everything Immediately

- Step Two Attempt a Chargeback Through Your Payment Provider

- Step Three Report to Financial Regulators

- Step Four Warn Other Traders Through Independent Reviews

- Step Five Be Cautious of Recovery Scams

- Frequently Asked Questions About Platforms That Refuse to Pay

Platforms that intend to refuse payments typically employ a predictable sequence of delay tactics when a withdrawal request is submitted. Initially they may cite verification requirements claiming documents are incomplete or insufficient even when these same documents were previously accepted without question.

As delays continue additional requirements may be introduced including requests for further documentation or explanations for the source of funds that were never mentioned during account setup. Fee requests framed as necessary processing charges or tax withholding requirements before funds can be released represent another common tactic since legitimate platforms never require payment to release client funds.

Eventually communication may become increasingly slow and unresponsive with responses growing shorter vaguer and less specific about when or how the issue will be resolved.

Step One Document Everything Immediately

As soon as you encounter any withdrawal obstacle begin documenting everything systematically. Save screenshots of all communications account balance displays trade history and any withdrawal requests submitted. Record dates and times of every interaction with customer support including the specific content of responses received.

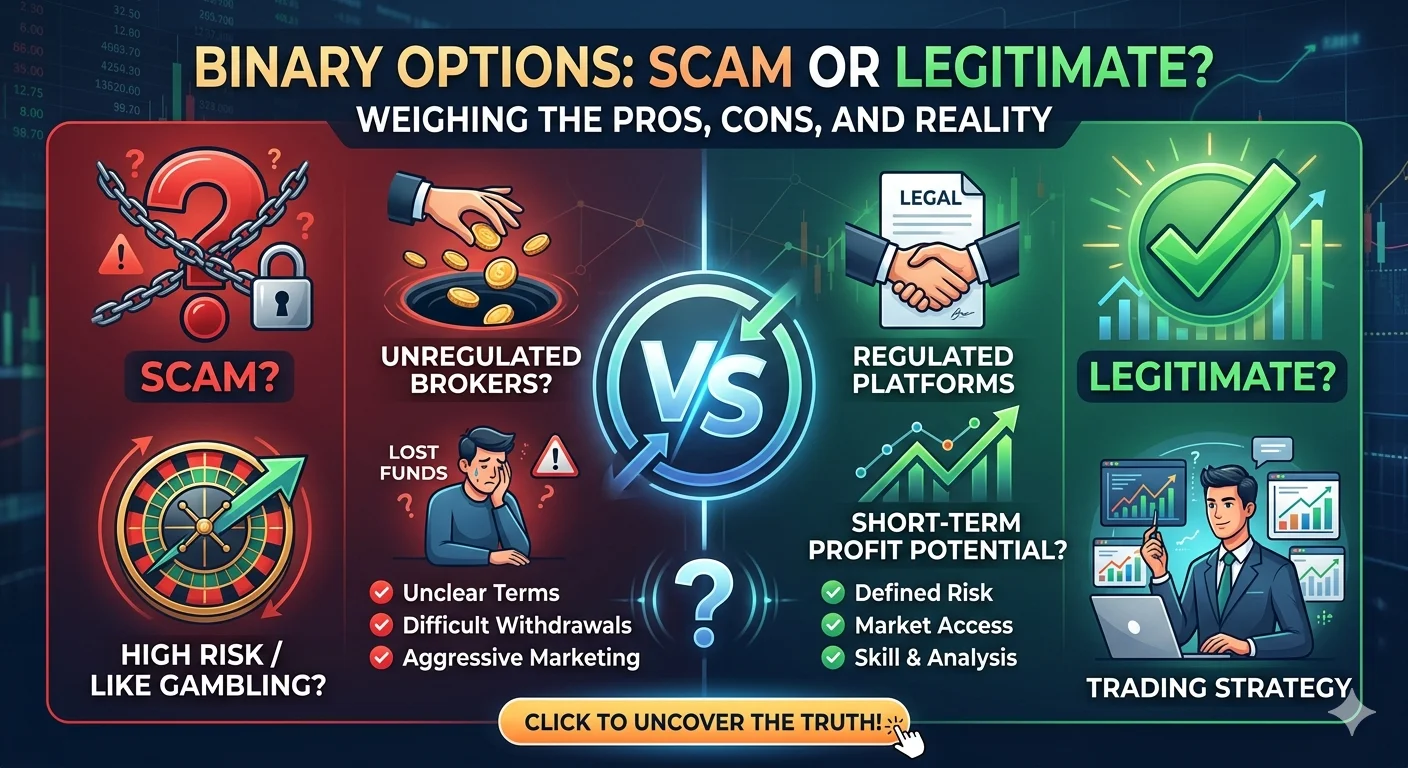

- Is Binary Options Trading a Scam or a Legitimate Way to Make Money

- Top Warning Signs of a Fake Binary Options Platform and How to Stay Safe

- How to Avoid Binary Options Scams and Spot Fake Brokers Before Losing Money

This documentation serves two important purposes. It strengthens any potential claim you make with your bank payment provider or financial regulator and it helps you track the progression of the platform's response pattern which can clarify whether you are dealing with a genuine processing delay or deliberate obstruction.

Step Two Attempt a Chargeback Through Your Payment Provider

If you funded your account using a credit or debit card contact your card issuer as soon as possible to inquire about initiating a chargeback for the disputed transaction. Chargebacks allow card issuers to reverse transactions when the agreed service has not been delivered which can apply in cases where a platform refuses to process a legitimate withdrawal.

Time limits apply to chargeback claims which vary by payment provider and card network so acting promptly after identifying a genuine withdrawal problem maximizes your chance of successfully using this option.

If you used an electronic payment system contact that provider's dispute resolution team with your documentation to explore what options may be available for your specific transaction type.

Recommended Articles

SCAM ALERTS

SCAM ALERTS

SCAM ALERTS

SCAM ALERTS

SCAM ALERTS

SCAM ALERTS

SCAM ALERTS

SCAM ALERTS

Step Three Report to Financial Regulators

Report the platform to relevant financial regulatory authorities in your country and in the country where the platform claims to be regulated. While individual regulatory complaints do not guarantee personal fund recovery they contribute to building a case against fraudulent operators and may trigger investigations that eventually result in action against the platform.

Search for the financial regulator relevant to your country using official government websites and submit a formal complaint with your complete documentation attached.

Step Four Warn Other Traders Through Independent Reviews

Share your experience on independent trading forums and review platforms to warn other potential victims. Fraudulent platforms depend on a continuous supply of new depositors to sustain their operation and honest detailed warnings from affected traders are one of the most effective tools for limiting the damage these operations can cause to others.

Be factual and specific in your warnings focusing on verifiable details such as dates amounts requested and specific responses received rather than emotional accusations that could undermine the credibility of your legitimate account.

Step Five Be Cautious of Recovery Scams

After experiencing a withdrawal refusal you may be approached by individuals or services claiming to specialize in recovering funds from fraudulent platforms often for an upfront fee. Many of these recovery services are themselves scams specifically targeting people who have already lost money to trading fraud.

Approach any unsolicited recovery service offer with extreme skepticism and never pay upfront fees to any third party claiming to recover your funds since legitimate legal and regulatory channels do not typically require advance payment of this nature.

Frequently Asked Questions About Platforms That Refuse to Pay

What should I do first if a platform refuses my withdrawal Document everything immediately including all communications and account information then contact your payment provider about chargeback options while simultaneously submitting a formal complaint to relevant financial regulators.

Can I always get my money back through a chargeback Not always. Chargebacks have time limits and eligibility requirements that vary by payment provider and transaction type. Acting quickly and providing clear documentation gives you the best chance of a successful outcome through this channel.

Are recovery services that charge upfront fees trustworthy Most are not. Unsolicited recovery service offers targeting people who have already experienced trading fraud are frequently scams themselves. Use official regulatory and legal channels rather than paying upfront fees to unverified third parties.

How long do I have to dispute a transaction with my card issuer Time limits vary between card networks and issuers but are often between sixty and one hundred twenty days from the original transaction date. Contact your card issuer as soon as possible to confirm the specific timeframe applicable to your situation.

Can reporting a platform to regulators help me recover my funds Regulatory complaints contribute to building cases against fraudulent operators though individual recovery through this channel alone is not guaranteed. Combined with payment provider disputes and other available channels the overall probability of some recovery improves.

Knowing which platforms have already been confirmed as scams helps you protect yourself before depositing. Continue reading our guide on the ten binary options platforms confirmed as scams you must avoid right now.

This article is for educational purposes only and does not constitute legal or financial advice. Always conduct your own independent research before depositing money with any trading platform.